“…the phrase “earning power” must imply a fairly confident expectation of certain future results. It is not sufficient to know what the past earnings have averaged, or even that they disclose a definite line of growth or decline.” ―Graham & Dodd, Security Analysis (6th Ed.)

Earning Power and Buffett’s 2015 Shareholder Letter

The concept of earning power was mentioned five times by Warren Buffett in his 2015 shareholder letter. It first appears on page four in Buffett’s review of the highlights of the year at Berkshire (emphasis added).

Charlie Munger, Berkshire Vice Chairman and my partner, and I expect Berkshire’s normalized earning power to increase every year. (Actual year-to-year earnings, of course, will sometimes decline because of weakness in the U.S. economy or, possibly, because of insurance mega-catastrophes.) In some years the normalized gains will be small; at other times they will be material. L

The second time Buffett talks about earning power in his discussion about Precision Castparts Corp., an acquisition that closed in the beginning of 2016.

Next year, I will be discussing the “Powerhouse Six.” The newcomer will be Precision Castparts Corp. (“PCC”), a business that we purchased a month ago for more than $32 billion of cash. PCC fits perfectly into the Berkshire model and will substantially increase our normalized per-share earning power.

The third time earning power is mentioned by Buffett is on connection to how future managers will proceed to build Berkshire’s intrinsic value.

Considering this favorable tailwind, Berkshire (and, to be sure, a great many other businesses) will almost certainly prosper. The managers who succeed Charlie and me will build Berkshire’s per-share intrinsic value by following our simple blueprint of: (1) constantly improving the basic earning power of our many subsidiaries; (2) further increasing their earnings through bolt-on acquisitions; (3) benefiting from the growth of our investees; (4) repurchasing Berkshire shares when they are available at a meaningful discount from intrinsic value; and (5) making an occasional large acquisition. Management will also try to maximize results for you by rarely, if ever, issuing Berkshire shares.

The fourth time is when Buffett discusses the importance of long-term debt as a founding source for the long-lived and regulated assets that Berkshire’s regulated, capital-intensive businesses own.

A key characteristic of both companies is their huge investment in very long-lived, regulated assets, with these partially funded by large amounts of long-term debt that is not guaranteed by Berkshire. Our credit is in fact not needed because each company has earning power that even under terrible economic conditions would far exceed its interest requirements. Last year, for example, in a disappointing year for railroads, BNSF’s interest coverage was more than 8:1. (Our definition of coverage is the ratio of earnings before interest and taxes to interest, not EBITDA/ interest, a commonly used measure we view as seriously flawed.)

The fifth, and last, time that earning power occurs is in connection to Buffetts discussion about how Berkshire managers think about how to grow their different businesses and adapt to changing circumstances in the competitive landscape.

Every day Berkshire managers are thinking about how they can better compete in an always-changing world. Just as vigorously, Charlie and I focus on where a steady stream of funds should be deployed. In that respect, we possess a major advantage over one-industry companies, whose options are far more limited. I firmly believe that Berkshire has the money, talent and culture to plow through the sort of adversities I’ve itemized above – and many more – and to emerge with ever-greater earning power.

So, Buffett clearly seems to focus on earning power as a highly important concept when it comes to looking at the different businesses in Berkshire’s possession. From having read the above quotations from the most recent shareholder letter, let’s have a closer look at the concept of earning power, and why it’s important to know be familiar with it.

The Power In “Earning Power”

In The Aggressive Conservative Investor Marty Whitman discusses the importance and implications of distinguishing between earnings and earning power.

Given the varied economic definitions of earnings, it may be wise to distinguish between earnings and earning power. By “earnings” is meant only reported accounting earnings. On the other hand, in referring to “earning power” the stress is on wealth creation. There is no need to equate a past earnings record with earning power. There is no a priori reason to view accounting earnings as the best indicator of earning power. Among other things, the amount of resources in the business at a given moment may be as good or a better indicator of earning power.

Graham & Dodd also put down their thoughts on earning power, for instance in Security Analysis (quotation below from the sixth edition).

Intrinsic Value vs. Price. From the foregoing examples it will be seen that the work of the securities analyst is not without concrete results of considerable practical value, and that it is applicable to a wide variety of situations. In all of these instances he appears to be concerned with the intrinsic value of the security and more particularly with the discovery of discrepancies between the intrinsic value and the market price. We must recognize, however, that intrinsic value is an elusive concept. In general terms it is understood to be that value which is justified by the facts, e.g., the assets, earnings, dividends, definite prospects, as distinct, let us say, from market quotations established by artificial manipulation or distorted by psychological excesses. But it is a great mistake to imagine that intrinsic value is as definite and as determinable as is the market price. Some time ago intrinsic value (in the case of a common stock) was thought to be about the same thing as “book value,” i.e., it was equal to the net assets of the business, fairly priced. This view of intrinsic value was quite definite, but it proved almost worthless as a practical matter because neither the average earnings nor the average market price evinced any tendency to be governed by the book value.

Intrinsic Value and “Earning Power.” Hence this idea was superseded by a newer view, viz., that the intrinsic value of a business was determined by its earning power. But the phrase “earning power” must imply a fairly confident expectation of certain future results. It is not sufficient to know what the past earnings have averaged, or even that they disclose a definite line of growth or decline. There must be plausible grounds for believing that this average or this trend is a dependable guide to the future. Experience has shown only too forcibly that in many instances this is far from true. This means that the concept of “earning power,” expressed as a definite figure, and the derived concept of intrinsic value, as something equally definite and ascertainable, cannot be safely accepted as a general premise of security analysis.

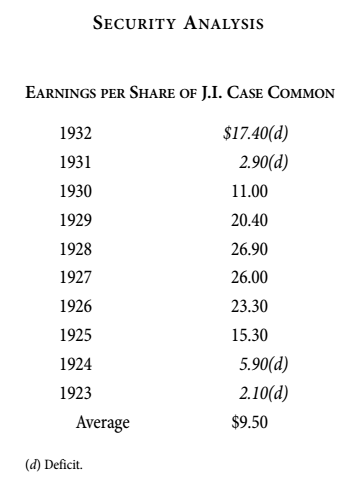

Example: To make this reasoning clearer, let us consider a concrete and typical example. What would we mean by the intrinsic value of J. I. Case Company common, as analyzed, say, early in 1933? The market price was $30; the asset value per share was $176; no dividend was being paid; the average earnings for ten years had been $9.50 per share; the results for 1932 had shown a deficit of $17 per share. If we followed a customary method of appraisal, we might take the average earnings per share of common for ten years, multiply this average by ten, and arrive at an intrinsic value of $95. But let us examine the individual figures which make up this ten-year average. They are as shown in the table on page 66. The average of $9.50 is obviously nothing more than an arithmetical resultant from ten unrelated figures. It can hardly be urged that this average is in any way representative of typical conditions in the past or representative of what may be expected in the future. Hence any figure of “real” or intrinsic value derived from this average must be characterized as equally accidental or artificial.

Warren Buffett: Earning Power Our Annual Goal

Today Buffett appeared on CNBC where he was interviewed by Becky Quick. One of the topics they talked about was earning power.

Becky Quick: Well, let’s start off talking with just the report itself in terms of how the businesses are doing. It was a strong year, profit was up sharply. How would you just state the overall business is doing right now?

Warren Buffett: Well most of the businesses did pretty well last year. And our goal is to add to the fundamental earning power every year. That doesn’t mean we think that earnings will go up every year, because sometimes you’ll be in recession or something of the sort. But we wanna feel at the end of the year we got more fundamental earning power on an average basis going forward than the start of the year. And since we retain all our earnings we ought to do that, it’s kind of silly to retain earnings just to stay flat. So every year, last year we were able to add a couple important businesses. They didn’t actually get done till after the year-end. And they will add to our earning power, and then we try to develop further the earning power of the businesses we already have, and that’s the goal year after year.

Becky Quick: The big addition for this year will be Precision Castparts.

Warren Buffett: Yeah, it didn’t close until about a month after the end of the year.

Becky Quick: You talk about the powerhouse five.

Warren Buffett: Yeah, now we’re gonna have the powerhouse six. And someday we’ll have the powerhouse eighty I hope.

Click image below to watch the interview.

S&P Earnings May Be Worse Than Advertised

Last Friday Herb Greenberg, Pacific Square Research, shared his perspective to why S&P earnings from 2015 may be worse than reported. Click image below to watch the interview.

Disclosure: I have a position in the BRK.B stock mentioned. I am not receiving compensation for it. I have no business relationship with the company. This article is informational and is in my own personal opinion. Always do your own due diligence and contact a financial professional before executing any trades or investments.

{kind=link}