Background: A framework of competitive advantages and some thoughts about Wal-Mart in 1974

This post is about Wal-Mart in the beginning of the 1970’s. The second part will look at Wal-Mart as of today.

Yesterday I read a post over at CSInvesting about analyzing Wal-Mart to try figuring out its competitive advantage and its nature.

“Let’s get back to Wal-Mart. What is the essence–the key–to its ability to grow profitably for so long? What can you spot in the 1974 annual report that would have – CSInvesting

First, I just read through it once. Then in the evening I had some time at hand so I picked up Wal-Mart’s annual report for fiscal year 1974 and then the annual report from 2012.

So, with this post I thought I would make an attempt to touch upon the question about any likely competitive advantages enjoyed by Wal-Mart in 1974 and its nature.

Business analysis is all about getting to know the fundamentals of a business as good as possible. Well, how then can one know if there is a competitive advantage present or not when looking at a business one might ask? I think the best answer to that question is that you have to know in some way what you’re looking for. You need a theoretical framework that contains different likely competitive advantages that a business may enjoy.

From there on, it’s all about reading about businesses, and then read some more. Reading is key. Focused reading is key. Pick a business or an industry, one at a time, and don’t move on until you feel that you know the fundamentals of the business or decide it’s too hard to figure out. Adopt the Charlie Munger approach “In,” “Out” and “Too hard.”

You have to go out and find the great companies, they will not come to you. Applying the theoretical framework containing the different competitive advantages helps you figure out if a specific business seems to enjoy any of the advantages. This will take time, but it will be great time spent because you will learn a lot. You will accumulate knowledge that you can use further on when looking at other businesses.

The key to investing intelligently is doing a thorough business analysis and to know what makes one business better than another. At the same time you have to keep your own feelings in check. As Richard P. Feynman once said “The first principle is that you must not fool yourself and you are the easiest person to fool.”

To start with, I want to make clear that I read Competition Demystified a few years back. I don’t know the exact words that it said about Wal-Mart, but I can say that the book analyzed Wal-Mart’s competitive position and I remember that the analysis was great. But, I won’t stay away from having another look just because I have already read the book. I just want to tell everyone that this book from Greenwald is definitely on my list of the best books to read to learn thinking about competitive advantages and strategy. It has influenced me a lot. So if my analysis is close to Greenwald’s, it’s because I read his book and learned a few things. If my analysis turns out not to be, I better go back and read Competition Demystified once again, because it is a great book that every business analyst and investor should read.

So, with this said. I think it’s time to take on Wal-Mart in 1974.

Wal-Mart’s annual report from 1974

Some notes from my reading of the 1974 annual report follows here:

- High and consistent growth in both revenues and earnings in 1970-74

- Revenues of $169.4 million (126.5 in 1973) and earnings of $6.2 million (4.6 in 1973)

- Number of stores at year-end was 78 (64 in 1973)

- Store locations concentrated to Arkansas, Missouri, Oklahoma (see map below) with distribution center right in the middle in Bentonville, the same place where its general office is located.

- “New stores scheduled during fiscal year 1975 will be within the 350 mile radius served by our Distribution Center.”

- “A new 150,000 square foot addition to our present distribution system is projected for this year, hopefully to be completed by September 1974. At that time, our total Distribution Center and General Office space will exceed 400,000 square feel.”

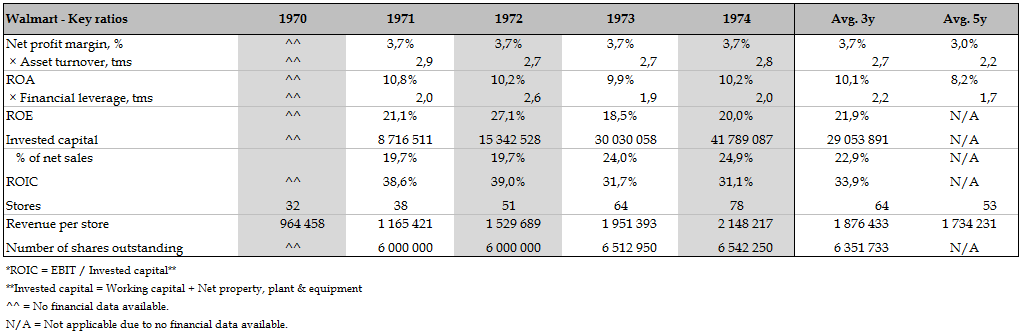

- See tables below for some financial data from the P&L, Balance sheet plus some financial ratios (click them to see better… I know it’s unreadable if you don’t)

- High returns on invested capital

- High and stable gross and operating margins

Here are some tables from the annual report that gives the reader a hint about the rapid and consistent growth in the years leading up to 1974.

From looking at the P&L the consistent growth coupled with high returns on invested capitals gives a hint that Wal-Mart seems to be doing something right. Three year average gross and operating margin were 26.4% and 7.7%.

A look at the balance sheet shows high growth in shareholders equity together with growing assets and debt. Growing at this high a growth rate requires capital. Even though the debt increased a lot, the whole business grew as seen by higher revenues converted to profits and also from looking at different lines in the balance sheet compared to net sales.

Return on equity was high, 20% in 1974 compared to a three year average of 22%. Return on invested capital (ROIC) was 31% in the same year, compared to a three-year average of 34%. Financial leverage was around 2 times and debt to equity was 0.36 and equity to total assets was 0.51 in 1974.

Likely competitive advantages and its nature

If I had to pick one picture to show from the 1974 annual report, it would be the map on page 8-9 showing all the store locations that are concentrated around the distribution center. Wal-Mart started off from Bentonville, from where it expanded its store locations and business operations. This concentration likely resulted in economies of scale in distribution and also in marketing.

Local concentration of store location – a powerful force in creating high returns

I have put together a list of the different kinds of competitive advantages a business may enjoy. From looking at Wal-Mart and going through the list (see table below), it seems reasonable to say Wal-Mart did not enjoy any cost advantages (i.e. superior production technology or privileged access to crucial inputs) above keeping costs low from operational efficiency. The same seems true for any government interventions.

So, from this, we go on to look if there seems to be any advantages from demand or economies of scale.

By looking at the map we see that stores are located close to each other in a cluster. This should give an advantage in distribution, advertising, and also in managing the stores, that a competitor with only a few stores in the same area wouldn’t be able to enjoy, at least not in the same extent. Wal-Mart’s focus on everyday low prices would probably also attract customers and hopefully keeping them from shopping elsewhere, so some habit formation here.

If we look at the different kinds of customer captivity, search costs are probably pretty low if not nonexistent. One has to assume that pretty much everyone could find out price levels in competing stores without investing too much time and effort. There might be some switching costs, in the sense that customers have to pay higher prices if they decide to go shopping at a competitor’s place.

When buying groceries most customers reasonably want two things, low prices and good (if not great) quality.

Groceries are bought periodically and it becomes a bit of a habit of going to the same store or chain. So, some customer captivity from habit seems reasonable to assume there is. But in the end a lot of people are willing to change stores to get even lower prices. So, as long as prices are low enough compared to competitors customers probably stay.

The most important thing in the grocery business is keeping prices low, to enjoy some customer captivity from habit and some switching costs. This becomes a feedback loop, with lower prices attracting more customers and more customers making it possible to keep prices at a low enough level.

Enjoying economies and scale, local in the case of Wal-Mart, and at the same time being able to attract a lot of customers means a business can spread its fixed costs (marketing, depreciation, distribution, management and other overhead expenses) over a greater revenue base, i.e. higher margins and returns on capital. This effect is also enhanced by the fact that stores are located in a limited area around the distribution center. Also, Wal-Mart looks to be operationally efficient in the way it conducts its everyday business, also a positive, even though it’s not considered a true competitive advantage.

To wrap this up, Wal-Mart in 1974 seems to enjoy competitive advantages from some customer captivity and local economies of scale (remember the map). If Wal-Mart where to expand into other areas these advantages would most likely be enjoyed by incumbent in these markets.

Having found a business enjoying a competitive advantage, the next question is about the sustainability of it. To say something about it, I am not really sure how one is supposed to proceed in trying to conquer Wal-Mart in this local area. So at least in the beginning of the 1970’s it should have been reasonable to expect Wal-Mart to keep its competitive advantages for some time in this local area where it operated, and by doing so protecting its profits from any potential entrants.

For a more thorough analysis of Wal-Mart’s competitive position in 1974 and its development from there, see Competition Demystified by Bruce Greenwald.